As China advances its carbon peaking and carbon neutrality goals and implements urban renewal and rural revitalization strategies, the sector is entering a new phase of high-quality growth centered on sustainability, smart technology, and service-oriented models. Industry data shows that China's mobile home market size has expanded from approximately 18 billion yuan in 2021 to nearly 32 billion yuan in 2025, achieving a compound annual growth rate (CAGR) of 15.4%. Market demand is projected to grow at an average annual rate of 18% from 2026 to 2030, with the total market size expected to exceed 70 billion yuan by 2030. Driven by policy guidance and technological innovation, the industry continues to optimize its product structure, broaden application scenarios, and accelerate market consolidation.

The continuous improvement of the policy system has laid a solid foundation for industry development. The Ministry of Housing and Urban-Rural Development's "14th Five-Year Plan for Construction Industry Development" explicitly requires that prefabricated buildings account for more than 30% of new construction area by 2025. Mobile homes, due to their high degree of prefabrication, rapid deployment, and recyclability, have become an important vehicle for achieving this goal. The value-added tax preferential policies for resource comprehensive utilization issued by the Ministry of Finance and the State Taxation Administration, as well as the measures taken by many regions to include mobile homes in the green building materials catalog and provide fiscal subsidies, have further reduced corporate costs and stimulated enthusiasm for green technology research and development. According to data from the China Building Metal Structure Association, in 2024, over 65% of mobile home manufacturers nationwide completed carbon verification or green factory certification, an increase of nearly 40 percentage points compared to 2020.

Technological innovation has become the key driver for enhancing the core competitiveness of mobile home independent stations.

By 2025, the industry is expected to achieve multiple breakthroughs in folding technology, smart systems, and eco-friendly solutions. In terms of folding and modular technology, the dual-wing folding house can be rapidly unfolded by 2-3 people in just 15-20 minutes. When folded, its volume shrinks to one-third of the unfolded state, reducing transportation costs by 30%-40%, while also being adaptable to diverse climates ranging from-20°C to 40°C.

In the green transition, the industry has established a complete low-carbon chain spanning material selection to full life cycle management. Companies widely adopt eco-friendly materials like high-strength lightweight steel and recycled aluminum, paired with green technologies such as photovoltaic-integrated roofs and rainwater recycling systems. This approach reduces carbon emissions during standardized mobile house construction by 45%-60% compared to traditional cast-in-place concrete structures, while cutting lifecycle carbon footprints by over 30%. Yazi Integrated Housing's modular products achieve a 90% reuse rate. In Sichuan's earthquake resettlement project, post-demolition reuse of components saved 950 tons of construction waste and reduced resettlement costs by 8 million yuan. Cutting-edge innovations also shine: capsule houses with IoT hubs enable smart control of lighting and energy systems, while flexible solar panels and micro wind turbines form off-grid micro-energy networks, making energy self-sufficiency achievable.

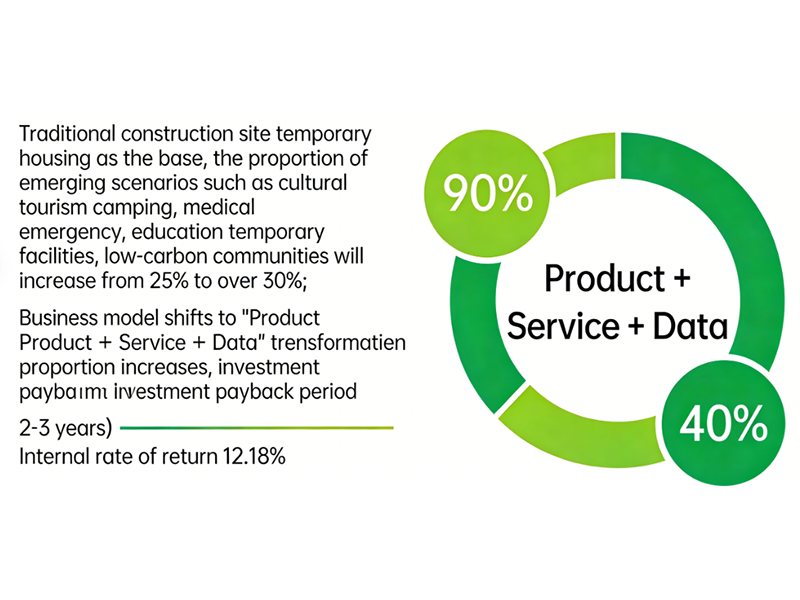

The market demand structure has undergone significant changes, with emerging scenarios becoming new growth engines. While temporary housing for traditional construction sites remains the market's foundation, demand for emerging sectors such as cultural tourism camping, medical emergency facilities, temporary educational infrastructure, and low-carbon communities is rapidly rising, with their combined share expected to increase from the current 25% to over 40%. In terms of regional development, East China and South China maintain leading advantages, while central and western regions are emerging as the most promising growth hubs due to policy incentives and urbanization progress. Business models have transitioned from single sales to integrated "product + service + data" operations, with rental models accounting for an increasing proportion year by year. Leading enterprises have established comprehensive service systems covering installation, operation, maintenance, and recycling, reducing typical project investment recovery periods to 2-3 years while maintaining internal rates of return (IRR) at 12%-18%.

Industry experts highlight that the mobile home sector currently faces risks including uncertainties in policy implementation, raw material price volatility, and homogenized competition. Moving forward, the industry must strengthen standard compliance capabilities, establish raw material hedging mechanisms, and enhance core competitiveness through differentiated innovation and digital operations. As the "Carbon Peak Implementation Plan for the Construction Sector" is fully implemented, the mobile home industry will accelerate its green and intelligent transformation, becoming a key driver for sustainable development in the construction sector while providing stable returns for investors and practitioners.